October 2025 Market Outlook

The third quarter of 2025 was marked by steady gains across equity markets as optimism about easing inflation and expectations for eventual Federal Reserve policy shifts outweighed lingering trade and geopolitical uncertainties. After the volatile rebound of Q2, investor sentiment remained resilient through the summer months. The S&P 500 advanced 8.1%, while the Nasdaq gained 11.4%, continuing to lead thanks to strength in AI, cloud, and semiconductor sectors. The Dow Jones Industrial Average rose a more modest 5.2%, reflecting steadier performance from industrials and financials. Despite ongoing uncertainty around a potential government shutdown, tariffs, and global trade policy, markets ended the quarter with momentum, supported by robust earnings in key sectors and an improving outlook for monetary easing in 2026.

Portfolio Highlights

During the third quarter, we maintained a constructive view on equities, with our core allocation to large-cap U.S. stocks unchanged. Although, the policy backdrop remains fluid, fiscal incentives from the recently passed “One Big Beautiful Bill Act,” a more accommodative Federal Reserve, and ongoing corporate earnings resilience all support this stance. International exposure was held steady, though we are incrementally favoring select small- and mid-cap opportunities where valuations remain compelling.

In fixed income, despite the Federal Reserve’s recent rate cut, we continue to take a more measured approach. We favor exposure to shorter maturities, which offer historically high income while reducing exposure to the risks created by heavy government debt issuance at the long end of the curve. This strategy allows us to generate attractive income today while preserving tactical flexibility to add duration when yields move towards the upper end of their range. We are also staying focused on high-quality credit and select opportunities in structured bonds that continue to offer favorable risk-reward profiles.

Looking ahead, the path of interest rates and the outcome of ongoing trade negotiations will be key drivers for markets in the final quarter of the year. While some volatility is likely, we believe a disciplined, diversified approach remains the best way to position portfolios for both opportunity and resilience.

Market Review

Markets extended their rebound in Q3 2025, buoyed by optimism around policy easing, strong corporate earnings, and further advances in AI and cloud infrastructure. The quarter opened with lingering volatility, but by mid-to-late Q3 sentiment turned decidedly more upbeat. The S&P 500 rose approximately 8.1%, led by strength in technology and consumer discretionary sectors, bringing its year-to-date return to roughly 14.4%. The Nasdaq outperformed with a 11.4% increase, powered by AI, cloud, and semiconductor names and is now up about 17.2% for the year. Finally, the Dow Jones Industrial Average gained 5.2%, reflecting more modest strength in industrials and financials and is higher by 9.2% year-to-date.

Large-cap growth and AI-linked names continued to lead, though breadth remained narrow. International equities, including emerging markets, also saw gains, aided by a weaker U.S. dollar and reduced trade tension. Defensive sectors and industrials lagged somewhat as rotational dynamics played out.

Going forward, risks include stretched equity valuations, concentration in mega-cap stocks, and any unanticipated inflation or policy surprises. But with clearer easing signals from central banks and generally solid corporate fundamentals, the tailwinds for equities appear more stable now than in prior quarters.

In fixed income, the 10-year U.S. Treasury yield began the quarter at 4.24%, climbed temporarily through July, before settling down at 4.15% by September 30th. This modest normalization reflected a recalibration between growth expectations and interest rate policy, which caused the yield curve to steepen slightly. Corporate credit spreads tightened over the period, signaling confidence in corporate balance sheets amid macro uncertainty.

The Fed and Looking Ahead

The Federal Reserve lowered its policy rate by 25 basis points in September, bringing the target range to 4.00%–4.25%. Policymakers signaled that this was the first step in a gradual easing cycle rather than the start of an aggressive cutting campaign. Inflation has continued to trend lower, though at 2.8%, Core PCE remains above the Federal Reserve’s long-term target. The labor market has cooled from its peak but continues to show resilience, with steady job growth and unemployment still near historic lows. However, there is concern about how much the lack of immigration is and will continue to affect these numbers. Chairman Jerome Powell reiterated that decisions would remain data dependent, balancing the need to support growth and employment with the ongoing risk that inflation proves sticky. Market expectations now align with up to two additional cuts by year-end, though uncertainty around the pace of disinflation and the fiscal backdrop keeps the path ahead less than clear. For investors, the takeaway is that while the Fed has begun to ease policy, the trajectory will likely be cautious and uneven as the central bank navigates between encouraging signs of cooling prices and persistent global uncertainties.

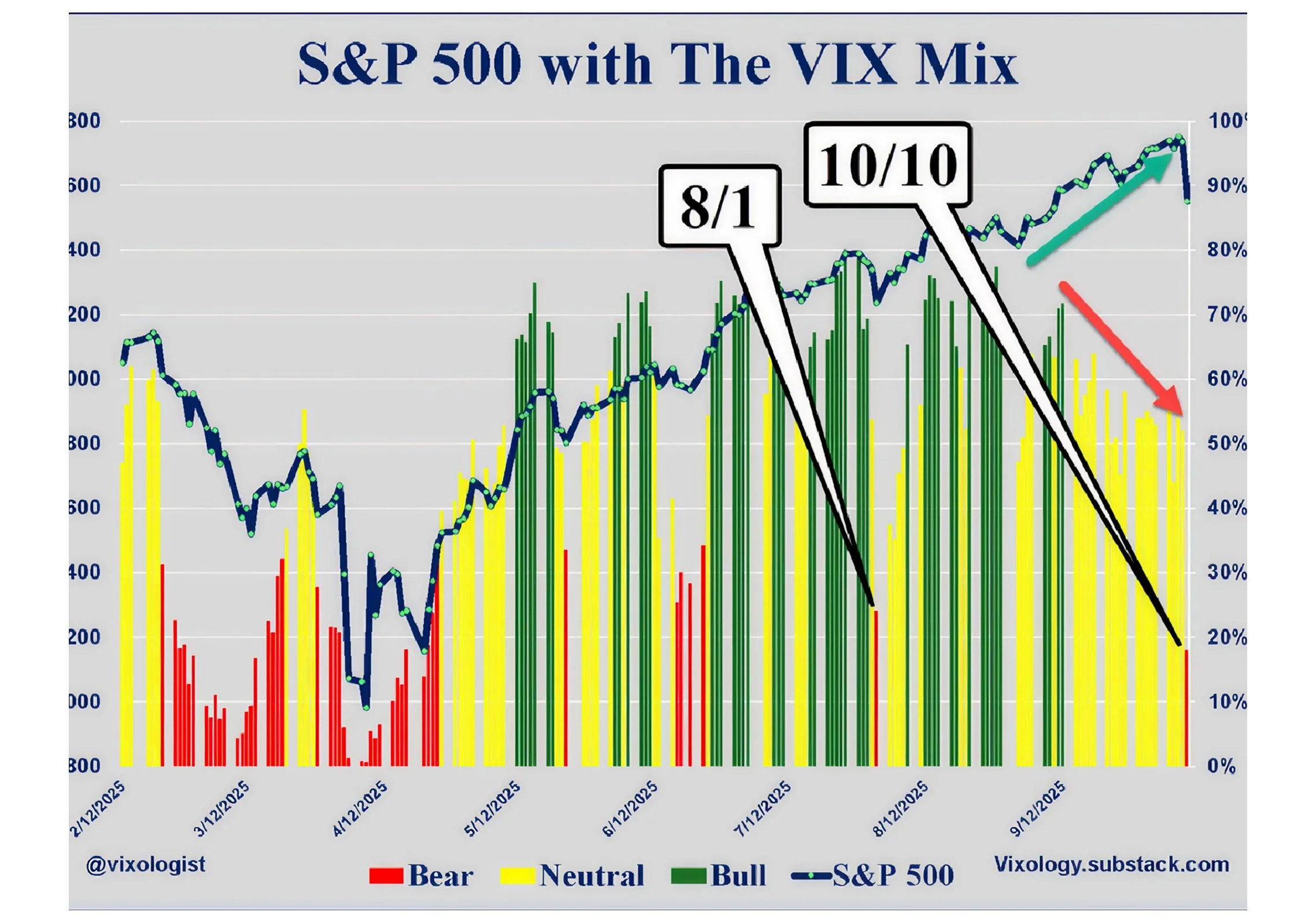

Volatility Corner

We can’t pretend to have predicted Friday’s volatility surge in response to President Trump’s social media post about a “massive” increase in tariffs on China after they announced further restrictions on rare earth metals. On the other hand, our daily commentary on Substack (vixololgy.substack.com) has been highlighting potential concerns over the past several weeks. Specifically, we’ve been pointing out that our proprietary volatility composite, the VIX Mix, had moved from bullish to neutral even as the S&P 500 and other US equity indices charted a series of new all-time highs. This divergence suggested that a significant number of investors were hedging their bets during the most recent leg of the rally that found its footing in late April and has seen buyers come in at every dip since then.

As shown below, Friday’s damage looks very similar to the abrupt pullback on August 1st in response to a weak jobs report and a previous tariff announcement. That proved to be a “one and done” as investors quickly rallied behind the uptrend in equities. This episode may well play out the same way, but it suggests that investors continue to be on edge and inclined to quickly head for the sidelines.

In Closing

Maintaining a diversified portfolio across asset classes remains essential for navigating today’s market volatility. Staying invested and avoiding reactionary decisions during periods of uncertainty continues to be a cornerstone of long-term success, particularly as geopolitical tensions and heightened tariff uncertainties play out.

Each investor’s risk tolerance and objectives are unique, so we encourage you to consult with your financial advisor to assess how this information might affect your overall investment strategy.

For more information, please email us at contact@ballastrockpw.com if you have any questions.